What Is Blockchain?

Most people believe blockchain started with Bitcoin.

The truth is very different.

Blockchain is not just a cryptocurrency technology.

It is the latest chapter in a 5000-year-old story.

A story about trust.

A story about records.

A story about how humans have tried to keep information safe, accurate, and verifiable for thousands of years.

Today blockchain powers Bitcoin, Ethereum, DeFi, NFTs, and Web3 applications.

But its roots go much deeper than cryptocurrency.

To understand blockchain, we must travel back thousands of years to the first civilizations in human history.

The World Runs on Records

Imagine waking up tomorrow and discovering that your bank balance has disappeared.

Or your property ownership records suddenly show someone else’s name.

Or your university degree cannot be verified.

How would you prove the truth?

The answer is simple.

You would rely on records.

Modern civilization runs on records.

Bank accounts are records.

Property ownership is a record.

Passports are records.

Stock ownership is a record.

Business transactions are records.

For thousands of years, humans have searched for better ways to protect these records.

Blockchain is simply the newest solution to an ancient problem.

The First Ledger in Human History

Around 3000 BCE, ancient Mesopotamian civilizations faced a challenge.

Trade was growing.

Merchants were exchanging grain, livestock, and goods.

But how could they keep track of everything?

The solution was surprisingly simple.

Clay tablets.

Archaeologists have discovered thousands of clay tablets containing trade records, tax records, loans, and ownership information.

These tablets became the world’s first ledgers.

A ledger is simply a record book.

This means blockchain is not a completely new concept.

The idea of maintaining records has existed for more than 5000 years.

The difference is that ancient ledgers were written on clay.

Blockchain ledgers are stored digitally across thousands of computers worldwide.

Luca Pacioli and Modern Accounting

In 1494, an Italian mathematician named Luca Pacioli changed finance forever.

He documented a system known as Double-Entry Bookkeeping.

Every transaction would have two entries:

- Debit

- Credit

This simple innovation dramatically improved trust in financial records.

Banks became stronger.

Businesses became more organized.

Global trade expanded.

Even today, modern accounting systems still use principles introduced by Luca Pacioli more than 500 years ago.

Blockchain is often described as the next major evolution in accounting and record keeping.

Computers Changed Everything

The arrival of computers in the 1960s and 1970s transformed record keeping.

Paper records became digital databases.

Information could be stored and processed faster than ever before.

However, one major problem remained.

Trust.

Digital databases still required a central authority.

A company.

A bank.

A government.

Someone had to control the records.

If that authority was compromised, the records could be altered, deleted, or manipulated.

This problem inspired a new generation of researchers.

One of them was David Chaum.

David Chaum: The Forgotten Genius

In 1982, computer scientist David Chaum published groundbreaking research on digital privacy.

He worried that future governments and corporations might track every online transaction.

His goal was simple.

Create a digital payment system that protected privacy.

Chaum introduced the concept of Blind Signatures, which allowed transactions to be verified without revealing personal identity.

Today he is widely considered one of the founding fathers of digital privacy.

But Chaum wanted more than theory.

He wanted a real-world solution.

That solution became DigiCash.

DigiCash: The Digital Money That Failed

In 1989, David Chaum launched DigiCash.

The vision was revolutionary.

Private digital money for the internet age.

Many experts believed DigiCash could transform online payments.

Banks partnered with the project.

Investors became interested.

Yet DigiCash failed.

Why?

Because it remained centralized.

The system depended on a company.

When the company failed, the entire system collapsed.

In 1998, DigiCash filed for bankruptcy.

The lesson was clear.

Digital money needed to survive without relying on a single company.

This lesson would later become a key part of blockchain design.

The Cypherpunk Movement

While DigiCash struggled, another movement was gaining momentum.

The Cypherpunks.

This community consisted of programmers, mathematicians, cryptographers, and privacy advocates.

Their mission was to protect freedom through cryptography.

In 1993, Eric Hughes published the famous Cypherpunk Manifesto.

One line became legendary:

Privacy is necessary for an open society in the electronic age.

Cypherpunks discussed digital money, encryption, privacy, and decentralized systems.

Many of the ideas that later shaped blockchain originated from these discussions.

Blockchain Is Born: The Breakthrough That Changed Everything

By the early 2000s, the world had already seen multiple attempts at creating digital money.

David Chaum had created DigiCash.

Wei Dai proposed b-money.

Nick Szabo introduced Bit Gold.

Adam Back developed Hashcash.

All of these ideas were important.

Yet none of them fully solved the problem.

The biggest challenge remained the same.

How do you create a digital system that works without trusting a central authority?

This question remained unanswered until 2008.

The year the global financial system experienced one of the biggest crises in modern history.

Banks were collapsing.

Governments were announcing bailouts.

Investors were panicking.

Public trust in financial institutions was falling rapidly.

And then something unusual happened.

On October 31, 2008, a nine-page document appeared on the internet.

The author called himself Satoshi Nakamoto.

The title was:

Bitcoin: A Peer-to-Peer Electronic Cash System

Most people focus on Bitcoin.

But the real innovation was the technology behind it.

Blockchain.

For the first time, someone successfully combined cryptography, distributed networks, and economic incentives into a system that could operate without a central authority.

Instead of trusting a bank, users could trust the network.

Instead of trusting a company, users could trust mathematics.

Instead of trusting a single database, users could trust thousands of copies spread across the world.

That was the breakthrough.

Blockchain solved a problem that researchers had been trying to solve for decades.

Why Blockchain Refuses To Die

One of the most fascinating things about blockchain is its ability to survive.

Many companies have failed.

Many exchanges have failed.

Many crypto projects have failed.

Yet major blockchains continue operating.

This happened because blockchain was designed differently.

Let’s look at some real examples.

The Mt. Gox Collapse

In 2014, Mt. Gox was the largest Bitcoin exchange in the world.

At one point, it handled nearly 70% of all Bitcoin trading activity.

Millions of users trusted the platform.

Then disaster struck.

Approximately 850,000 Bitcoin went missing.

The exchange collapsed.

News headlines declared:

- Bitcoin is dead.

- Crypto is finished.

- The experiment has failed.

But something interesting happened.

Mt. Gox died.

Bitcoin did not.

The exchange failed.

The blockchain survived.

This taught the world an important lesson.

An exchange is not the blockchain.

A company can disappear.

A blockchain network can continue operating.

The China Mining Ban

For many years, China dominated Bitcoin mining.

Before 2021, a large percentage of global Bitcoin hash power was located inside China.

Then Chinese authorities launched a major crackdown.

Mining farms were shut down.

Machines were removed.

Thousands of miners were forced to relocate.

Many people believed this would permanently damage Bitcoin.

Instead, the network adapted.

Miners moved to:

- United States

- Kazakhstan

- Canada

- Russia

- Other regions

Hash rate recovered.

The network continued running.

This demonstrated one of blockchain’s most important strengths.

Decentralization.

No single country controlled the network.

No single government could shut it down completely.

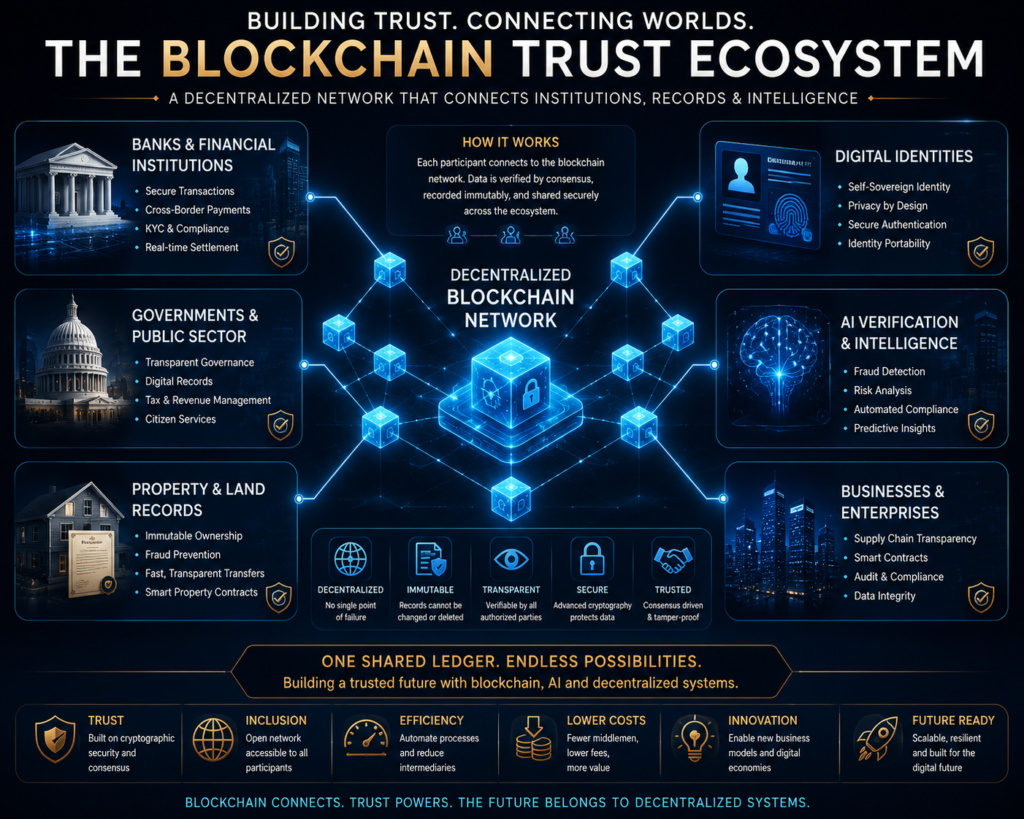

Blockchain Beyond Bitcoin

Many people still associate blockchain only with cryptocurrency.

However, blockchain applications now extend far beyond Bitcoin.

Developers, governments, and corporations have explored blockchain for:

- Supply chains

- Digital identity

- Property records

- Healthcare systems

- Voting systems

- Asset tokenization

The goal is simple.

Create records that are transparent, secure, and difficult to manipulate.

Not every blockchain project succeeds.

But the technology continues to attract interest because trust remains a universal challenge.

India and Blockchain

India has become one of the world’s largest digital economies.

UPI processes billions of transactions every month.

Digital payments have become a part of everyday life.

As digital activity grows, record verification becomes increasingly important.

This is where blockchain enters the discussion.

Several blockchain pilot projects have been explored in India for:

- Land records

- Supply chain tracking

- Education certificates

- Government services

Blockchain is not replacing existing systems overnight.

However, many experts believe it could improve transparency and verification in specific areas.

India’s interest in blockchain reflects a larger global trend.

The search for more trustworthy digital infrastructure.

Digital Rupee and Blockchain

The rise of Central Bank Digital Currencies (CBDCs) has also increased interest in blockchain-related technologies.

India’s Digital Rupee initiative demonstrates how governments are exploring the future of digital finance.

It is important to understand that:

Bitcoin and Digital Rupee are not the same thing.

Bitcoin is decentralized.

Digital Rupee is centrally managed.

Yet both reflect the growing importance of digital financial systems.

The future of money is becoming increasingly digital.

And blockchain remains a major part of that conversation.

AI and Blockchain: The Future of Trust

Artificial Intelligence is transforming the world.

AI can now:

- Generate images

- Create videos

- Clone voices

- Produce realistic content

While this is exciting, it creates a new challenge.

Verification.

How do we know what is real?

How do we verify ownership?

How do we verify identity?

This is where blockchain may play a major role.

Many researchers believe AI and blockchain could work together.

AI creates information.

Blockchain verifies information.

Imagine a future where:

- Educational certificates are verified on blockchain.

- Property ownership is permanently recorded.

- Digital identities are secured.

- AI-generated content can be authenticated.

This future is still evolving.

But it demonstrates why blockchain remains one of the most important technologies of the digital age.

Final Thoughts

Blockchain is often described as the technology behind Bitcoin.

That description is true.

But it is incomplete.

Blockchain is part of a much larger story.

A story that began more than 5000 years ago with clay tablets in Mesopotamia.

A story that continued through accounting systems, databases, digital money experiments, and cryptography.

A story about trust.

Every generation has searched for better ways to protect information.

Blockchain is simply the latest chapter in that journey.

Whether blockchain ultimately becomes the foundation of future digital systems remains to be seen.

But one thing is clear.

Its impact on technology, finance, and digital innovation has already secured its place in history.

Bitcoin may be blockchain’s most famous application.

But blockchain’s story is much bigger than Bitcoin.

Also Read

To understand the technology behind this digital revolution, read our What Is Blockchain? Complete Beginner Guide.

Blockchain became famous because of Bitcoin. Learn the full foundation in our What Is Bitcoin? Complete Beginner Guide.

If you want to know how blockchain records transactions, read our guide on How Cryptocurrency Transactions Work on Blockchain.

To understand the next evolution after Bitcoin, read Ethereum Story: How Vitalik Buterin Created Ethereum and Changed Crypto.

For a deeper look at crypto adoption by major institutions, read BlackRock History: How Larry Fink Built a $11 Trillion Financial Giant.

Also Read

Bitcoin WhitepaperEthereum Official Website

Reserve Bank of India (RBI)

IBM Blockchain Solutions

FAQ

What is blockchain in simple words?

Blockchain is a digital ledger that stores information across multiple computers, making records secure, transparent, and difficult to alter.

Who invented blockchain?

The blockchain system used in Bitcoin was introduced by Satoshi Nakamoto in 2008, but many earlier researchers contributed ideas that made blockchain possible.

Is blockchain only used for cryptocurrency?

No. Blockchain can be used for digital identity, supply chains, property records, healthcare, and many other applications.

Why is blockchain important?

Blockchain helps create trustworthy records without relying on a single central authority.

What is the difference between Bitcoin and blockchain?

Bitcoin is a cryptocurrency.

Blockchain is the underlying technology that powers Bitcoin and many other systems.

join our Telegram for instant crypto updates.

Subscribe to our youtube Channel

For detailed crypto market analysis, price predictions, and investment strategies,

subscribe to our YouTube channel Coin Alert

For more beginner-friendly crypto education, in-depth guides, and documentary-style crypto stories, visit Coin Alert regularly.

🌐 Website: https://coinalert.in

📢 Telegram: https://t.me/coinalert

Stay informed. Stay secure. Learn before you invest.

Dr. Khushwant Rana is the founder of Coin Alert and has 15+ years of business experience. He creates beginner-friendly crypto educational content focused on Bitcoin, blockchain, Web3, crypto security, and real-world crypto awareness in India.